5 Steps to make the monthly payment for tax contribution for salary is as follows. Applications are to be made to MIDA by 31 December 2021.

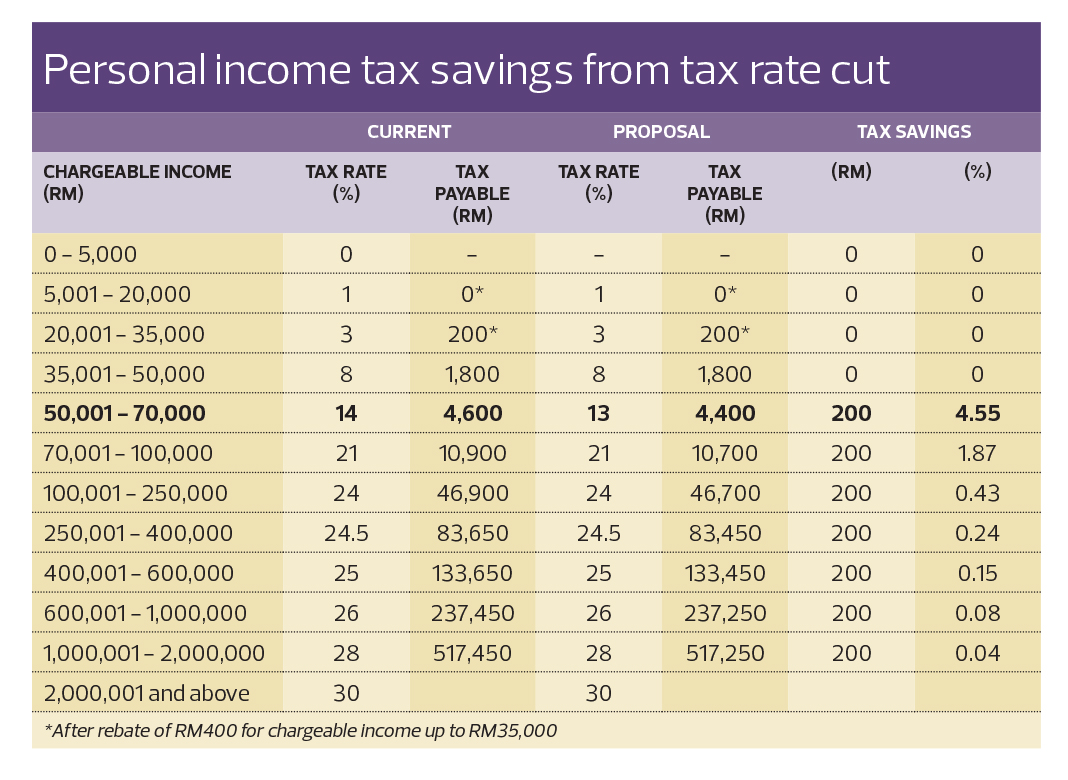

Budget 2021 Tax Reduction For M40 Timely Yet More Could Be Done The Edge Markets

1 Section 3A states that a Labuan entity carrying on a Labuan business activity may make an irrevocable election in the prescribed form so that any.

Personal income tax labuan. According to Section 41 of LBATA tax shall be charged at a rate of 3 a year on the net audited profits of a Labuan entity carrying on a trading activity. Interest paid by a resident Labuan company to a non-resident are subjected to a withholding tax rate of 15. As long as your Malaysian counterpart willing to accept the non-deductibility as mentioned above Labuan company is entitled to the tax rate according to the latest Labuan Tax 2019 law.

Short-term visitors to Malaysia are exempt from income tax if their employment does not exceed. Tax return is up to date till year assessment 2019. Malaysia Double Taxation Agreement DTA protects your income from being taxed twice.

Contract payments to non-resident contractors 10. - Under Section 3A1 of the LBATA 1990 a company can elect to be taxed under the Malaysia Income Tax Act 1967 ie. Register Labuan Company for Employer File E number with the Inland Revenue Board IRB Determine if the employee foreign director expatriates locals has the monthly income more than RM2850 threshold for.

Flat personal income tax rate of 15 for a continuous period of 5 YAs on his her income derived from exercising employment with a Malaysian resident. Foreign sourced income received in Malaysia by resident individuals are tax-exempt. Mon - Thu.

Labuan holding company is subject to 0 tax zero tax Labuan licensed company is subject to 3 tax. Local-resident tax status stay 182 daysyear in Malaysia the tax rate will range from 0 -28 of the net income Non-resident tax status stay tax rate will be 28 flat of the net income. 087 - 415 385.

Latest Labuan Company Tax- Employers Return and Personal Income Tax Every Labuan company is obliged to comply with IRBs regulations to lodge Employer Return Form LE declaring the number of staffs employed in the Company and every employee has the duty to file their Personal Income Tax Form BE on yearly basis. Fees paid by a resident Labuan company to a non-resident for onshore services andor use of moveable property is generally subjected to a withholding tax rate of 10. 50 of the gross employment income received by an individual non-Malaysian citizen in a managerial capacity with a Labuan entity in Labuan co-located office or marketing office is exempted from income tax from YA 2011 to YA 2020.

Labuan Taxes are Easy. Individuals Individual residents in Labuan with income accruing in or derived from Malaysia are subject to tax. Royalties paid by a Labuan corporation to a non-resident are subjected to a 10 withholding tax rate.

The remaining balance of 40 must be applied straight to 28102020 one time application and must be. THE LABUAN TAX FRAMEWORK The tax laws relating to Labuan entities are set out in the Labuan Business Activity Tax Act 1990 LBATA. Other Labuan tax and.

All directors and employees working at Labuan Company are required to submit a personal income tax return to the Internal Revenue Service IRB for salary income earned in the previous calendar year. The Labuan Income Tax Office LHDN Labuan is one of the main revenue collecting agencies of the Ministry of Finance. Apply for Labuan work permit dependent pass while working for a Labuan company.

Alternatively you may also opt to pay a 24 tax rate dealing with Malaysian companies. Kindly note that the deadline for declarations is until April 30th. The Labuan Financial Services Authority Labuan FSA formerly known as Labuan Offshore Financial Services Authority LOFSA is an agency established on 15 February.

Co-located office means on office of a Labuan entity approved by the Labuan Financial Services Authority which operates in other parts of Malaysia to perform the functions assigned by the Labuan. Royalties for the use or conveyance of intangible property 10. Please refer to the guidelines for the required documents and application process.

Services of a public entertainer 15. Labuan entities carrying on a Labuan trading activity no longer have the option to elect to pay tax of RM20000. Personal services associated with the use of intangible property 10.

For Malaysians the personal income tax filing is only applicable to. Only applicable for Labuan Entity that has no tax outstanding including compound and tax increment. The rate of tax ranges from 0 to 28 for resident individuals and a flat rate of 28 for non-resident individuals.

800am - 1215pm 245pm - 500pm. Subject to corporate tax rate of 20 on the first MYR500000 and thereafter 24. Income derived from royalty or other income derived from an intellectual property right shall not enjoy LBATA tax and is now subject to tax under the Malaysian Income Tax Act 1967.

More on Personal Tax Incentives for Labuan Expatriates. 800am - 100pm 200pm - 500pm.

Http Www Mymoneyblog Com Images 0902 Scorp Gif Self Employment Income Tax S Corporation

Old Or New Tax Slabs For Fy 2020 21 Amount At Which Tax Are Same Incometax Budget Unionbudget2020 Oldvsnew Income Tax Indirect Tax Budgeting